The Secure Act 2.0 is now law in the U.S.

This new legislation has features that many deem to be positive. But the rules pertaining to required minimum distributions (RMDs) warrant your close attention. They can have some unintended consequences that could be very costly to your retirement.

Are there ways to plan around this so your retirement dreams don’t blow-up in your face? That’s what we’re going to talk about here.

A quick history…

Back in 2020 and before, you had to start taking required minimum distributions from your traditional retirement accounts by age 70 ½.

A couple of years ago with the first Secure Act, the government raised the RMD age to 72. With Secure Act 2.0, the age bumps up to 73 and rises to age 75 in 2033.

At first glance, this all seems great. It allows your investments to grow tax deferred even longer. Plus, the length of time that you can contribute to tax deferred retirement accounts has been extended. On the surface, it all sounds good. So, what’s the problem?

The issue of a “smaller window”

One of the unintended consequences of Secure Act 2.0 is that you now have a smaller window of time to take distributions from your traditional balances.

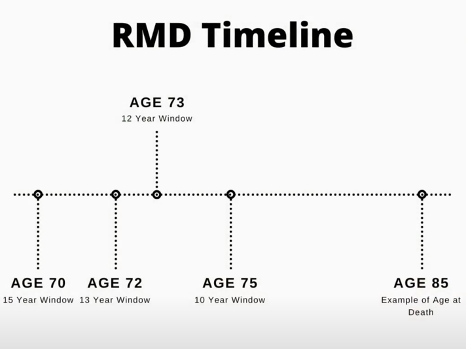

For example, look at this RMD Timeline showing someone who is currently 70 and lives to be 85.

Under the old system, this individual would have a 15-year window in which to take required minimum distributions—from age 70 to age 85.

With the original Secure Act, the government raised the RMD age to 72, leaving a 13-year window in which to take distributions.

Now, the age is rising to 75, which will leave only a 10-year window for individuals to take distributions.

Why does this matter? Because the older you are, the higher the percentage you have to take out.

Ed Slott is considered America’s IRA expert. (He’s actually a CPA and not a financial planner, but he does a lot of research on taxes.) Here’s what he says:

“The more you push back on the RMD age, the shorter that window to get all the money out becomes. And as you stuff more income into a shorter time overall, you and your beneficiaries are going to end up paying more in taxes.”

Affecting your Social Security?

One of the unintended consequences of Secure Act 2.0 is increased taxes on Social Security.

How does taxation of Social Security work in the first place? Social Security is taxed based on your combined income. You have to add your adjusted gross income (AGI) plus any non-taxable interest received from investments, plus 1/2 of your Social Security benefits.

If that totals less than $25,000 (married filing jointly), you pay zero tax on your Social Security benefits. However, if your combined income is between $25,000-$34,000, you have to pay taxes on 50% of your Social Security income. And if your income is over $34,000, then 85% of your Social Security income is subject to taxation.

Obviously, being forced to take higher RMDs over a shorter period of time increases your income. And if that additional income pushes you over these limits, then you face even more taxation on your Social Security—taxes that otherwise you wouldn’t have owed.

In short, if you delay taking your funds until age 75, it increases the chances you will have to pay a higher tax bill.

Higher Medicare premiums?

The next potential negative impact is on your Medicare premiums. We did a whole video on “Can RMDs Increase your Medicare Premiums?” and—spoiler alert—yes, they can.

In 2023, the minimum Medicare premium is $164.90. To qualify for that premium—if you’re married filing jointly—your income has to be less than $194,000.

If your joint income falls between $194,000 and $246,000, the price of Medicare rises to $230.80 a month. Make more than $246,000 jointly, and you’ll pay $329.70 a month, which is double a standard Medicare premium.

In short, if your income increases because you’re required to take out larger distributions, it may cause you to pay higher Medicare premiums.

The problem of higher account balances

Another pitfall of the new Secure Act 2.0 is that if you delay your distributions, in theory, your traditional account will be larger. That’s because over the long-haul, investments in the markets tend to grow. (Of course, this depends on how aggressive or conservative you are, and how you have your investments set-up.)

This means that by waiting until RMD age, and by having a larger traditional balance, you’ll have to take out more money because you have less time to take your distributions.

As we’ve shown, this can raise taxes on your Social Security benefits. It can also make your Medicare premiums go up. What else can it do? It can make your taxable income as a whole higher.

A higher overall tax bill?

Think about those future retirees who wait until age 75 to start taking RMDs. They may already have a federal pension that includes cost of living raises up to age 75. The same goes for the Social Security checks they’re receiving. Obviously, a retiree’s monthly income rises each time they get a cost of living adjustment (COLA).

Now, at 75, they’ve got to start taking RDMs too. Because they haven’t touched these investments previously, these accounts are likely to have larger balances. And now, because they’re older, these retirees must take a higher percentage of this money.

Here’s why that’s not ideal: RMDs from traditional accounts are completely taxable. Perhaps prior to receiving any RMD money annually, you were in the 22% bracket. Suddenly, at 75, you may find yourself in the 24% bracket! Or maybe you would’ve been in the 24% bracket, but now thanks to that RMD money, you’re going to be in the 32% bracket!

Do you see how being forced to take larger distributions out over a smaller window of time can cause you to slide up into a higher tax bracket? If you’re not careful in your planning you could end up paying higher taxes!

Another potential problem has to do with tax rates when you’re 75. We know what tax rates are today, but who can say what they’ll be when you turn 75? If taxes are higher, it just amplifies the potential problems of Secure Act 2.0.

Consequences for your heirs?

Another issue involves what you’re doing for your heirs. Prior to 2020, someone could inherit an IRA and do what’s called a “stretch IRA.” (That’s where heirs take a minimum amount out for the rest of their lives.) So, for example, you could leave a $1 million IRA to your children, and they could stretch it out for 40 years–and avoid a big tax hit–by taking small amounts out annually.

That rule went away with the first Secure Act. Now if someone—other than your spouse—inherits your IRA, they have a 10-year window to withdraw the money.

This creates the same problem we talked about earlier—having to withdraw a large amount of money over a small number of years. Imagine inheriting $1 million—all of it taxable—and having to take it out over a ten-year period.

At first glance you think, “It’s a million dollars, and they have 10 years. They can just take $100,000 a year.” But it’s not quite that easy. What if that $1 million account is growing at 5% per year? That means the heir(s) would actually have to take out $129,000 annually to withdraw all the money over a decade.

Some people think, “Who cares if it’s taxable? If my kids get even ⅔ of that money, they should be happy!” But remember, we’re trying to plan as efficiently and effectively as we can. We don’t want our heirs paying exorbitant taxes if we can avoid it.

Remember something else: It’s likely that your children will be inheriting this money during their peak earning years. So, whatever their taxable income would have been, it’s now going to be $129,000 higher every year—thanks to the RMD rules. Do you think that will push them up into a higher tax bracket? Absolutely, it could!

So, we see four unintended consequences of the RMD requirements of Secure Act 2.0:

- Higher taxation on your Social Security

- Higher Medicare premiums

- Higher tax bracket

- Heirs taxed at higher rates

That’s the bad news. The good new, however, is this: People who plan carefully and strategically can avoid many of these potential RMD problems.

An example of how planning can help

Here’s one example of how smart planning can save thousands (using the fourth issue listed above).

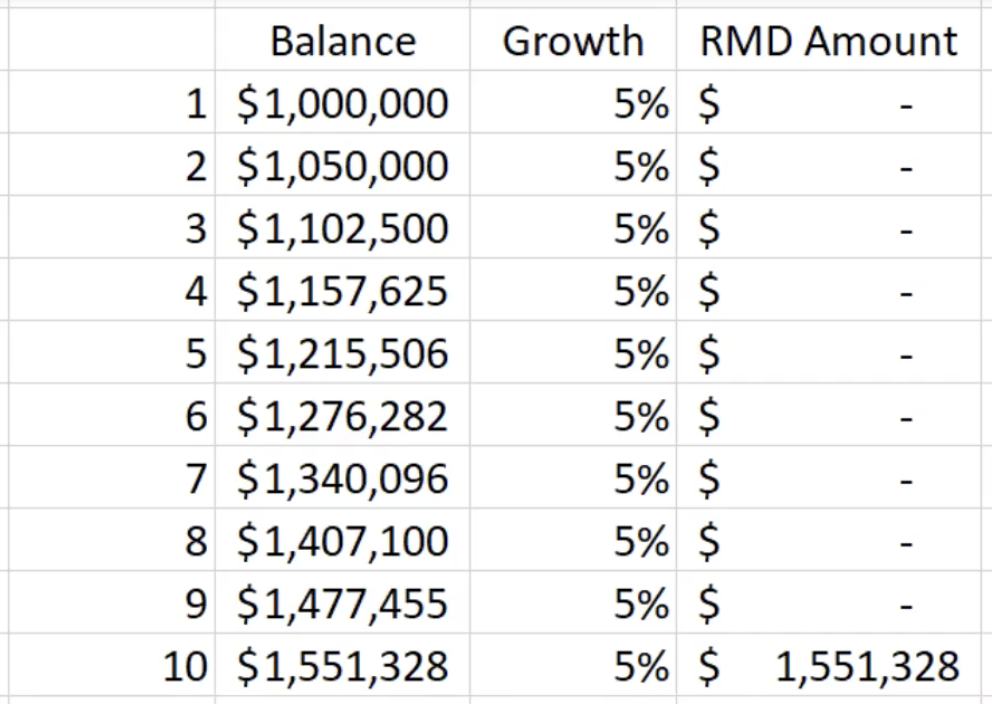

Let’s say, upon your death, your heirs get a $1 million Roth account instead of a $1 million traditional account. They still would be subject to RMD rules. But their distributions would not be taxable.

Look at this table and see the difference. With a Roth account, it no longer makes sense to pull out an even amount each year. Because this is all Roth money, your heirs may wish to let it grow tax-free as long as possible.

If they withdrew it all in the 10th year, they could take $1,551,328, and it would all be tax-free!

With a traditional account, your heirs would pull out a total of $1,290,000 over 10 years ($129,000 a year) and it would all be taxable. With a Roth account, they’d be pulling out over $1.5 million, and none of it would be taxable!

To avoid RMD problems at age 75, you have to keep your traditional balances from getting bigger and bigger and bigger. One smart way to do this is by doing Roth conversions.

The advantage of Roth conversions

A Roth conversion is where you take an appropriate portion of your traditional money and move it into a Roth account. (NOTE: Since the amount of money you move each year is taxable, you always want to consult first with your financial advisor and/or your CPA).

The following year you can do this again, and each year following, until you eventually get all of your traditional money—or at least a majority of it–into a Roth account. (See a more detailed video here on this subject: “Should you Roth Convert All of Your Money?”).

A side note: If you wish to give money to charity, you may choose to give that as traditional money and not as Roth money. When you give to charity using a qualified charitable deduction (QCD), no one pays the tax. (That’s a separate discussion for another day and another video/blog post).

Back to Roth conversions…how exactly does one do them? It’s important to know you can’t do a Roth conversion straight from your TSP or your 401(k) with your employer. You cannot go into your TSP and take $100,000 and move it to Roth inside the TSP. That’s not allowed.

To do a Roth conversion, you first have to move the TSP or 401(k) money out into an IRA. When can you do this? You either have to be 59 and ½ and still working or retired.

We talk in greater detail about the best way to do all this in our video “Can I contribute to both Roth TSP and Roth IRA in the same year?” You can watch it here.

Do you have other questions about RMDs or other issues of retirement? In the upper right-hand corner, you’ll see a button that says Talk with an Advisor. Click there and you’ll be able to send us a short email message. We promise to contact you promptly. Or, if you’d like to speak with an advisor right now, our number is (866) 331-7749. Give us a call.

You don’t have to wonder or guess at your financial future. We can help you take the mystery out of retirement.