It’s time we talked about RMDs.

I don’t mean “Really Messy Desks” or “Rapidly Melting Desserts.” (Though both of those realities are problematic and worth discussing.)

I’m referring to Required Minimum Distributions. Simply put, that’s the amount of money the government says you must take out of your retirement savings account each year once you reach a certain age. Tax laws force us to do this so the government can finally collect taxes on all the money we’ve been stashing in our traditional IRAs (Individual Retirement Accounts) or TSPs (Thrift Savings Plans).

(Now you know why some insist that RMD really stands for “Ridiculous Money Demand.”)

The best way to understand RMDs is to answer the questions we often hear about them. Here are the 10 we get most frequently:

1. When do my RMDs start?

It used to be age 70 1/2. But now if you were born July 1, 1949 to December 31, 1950, your RMD age is 72. If you were born from January 1, 1951, to December 31, 1959, your RMD age is 73. For anyone born after January 1, 1960, your RMD age is 75.

2. How are my RMDs calculated?

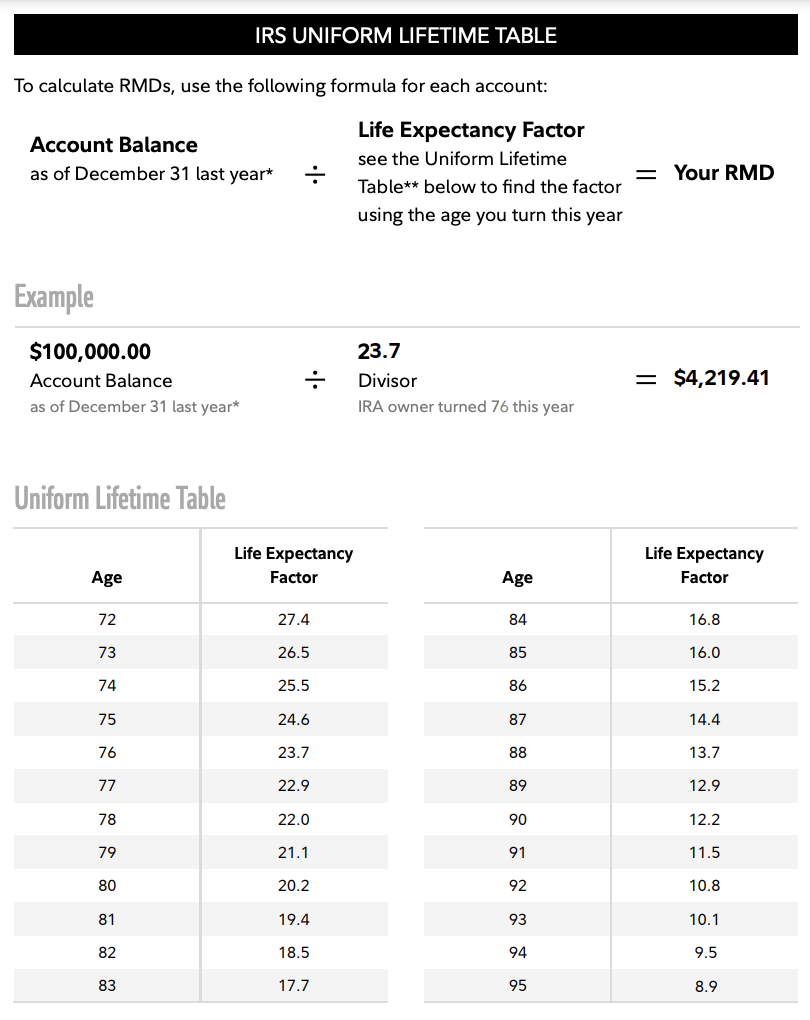

The uniform lifetime table is the most used.

You can see here there’s the age and then there’s a life expectancy factor. Here’s how it works: You take the December 31 end-of-the-year balance of your traditional retirement accounts and you divide by the factor.

Let’s say you have $1 million in traditional IRAs, and you are 75 years old. Divide that by 24.6 and you come up with $40,650. That’s the amount that you will be required to withdraw from your traditional accounts. You can see that each year, the life expectancy factor is going down and the lower that number, the larger the required minimum distribution will be.

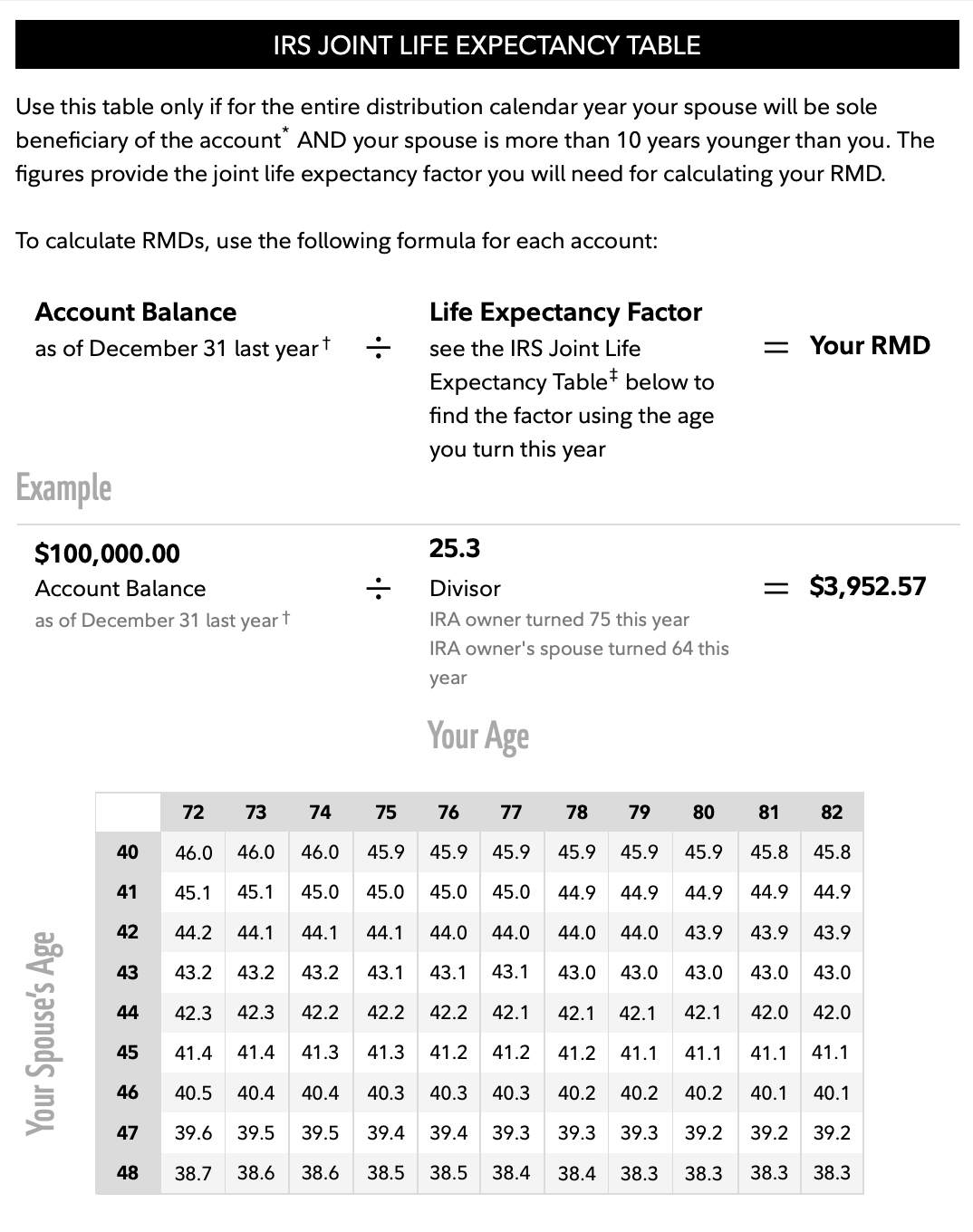

They also have a joint life expectancy table. It is used if your spouse is your sole beneficiary and your spouse is more than 10 years younger than you. So with this chart, you take your age and your spouse’s age and the spot where they meet is the factor you use.

You do the same thing where you take your IRA balance as of December 31 of the prior year and you divide by the life expectancy factor. Notice here on the joint life, that these numbers are larger, and the larger the factor, the smaller the required distribution will be. Most people want their RMD to be as small as possible. If that’s true for you, you may want to use the joint life table.

3. Do I have to take an RMD the first year?

You don’t have to take your first RMD by December 31. You have until tax day in April of the following year. So, if you wait until, let’s say, March or April to take the previous year’s RMD, you’ll have to take two RMDs in that second year. After the first year, you’ll always face a December 31 deadline. Depending on your income situation, it may make sense to delay and have two RMDs in the following year. Or, it may make sense to not delay and go ahead and take one this year so that you don’t have to double up in year two.

4. Are there RMDs from Roth IRA or Roth TSP?

No. You only have to take RMDs from traditional retirement accounts. The theory behind it is that the IRS has not taxed your money yet, and so they force you to start taking money out of the taxable money, but they don’t force you to take it out of Roth. And we have lots of other videos on how to reduce RMDs. One way to do that is to move money to your Roth account year after year by doing Roth conversions. Some people want to do this effectively enough so that when they show up at their RMD age, they don’t have any traditional accounts which means they won’t have any required minimum distributions. This is one advantage I think that Roth has over traditional in that no one forces you to take distributions.

5. Can I aggregate my RMDs?

That’s just a fancy way to say, “Do I have to take an RMD from each individual account I have, or can I just add up all the balances and figure out my total RMD and take it from one account?”

The answer is yes and no. With IRAs, yes, you can aggregate. You don’t have to take a minimum distribution from every IRA you have. You can add up the total, figure out the amount, and take the distribution from one IRA.

Keep in mind this does not work for spouses. The husband can aggregate his accounts and take one RMD, and the wife can aggregate hers and take one RMD. You cannot take all RMDS for both husband and wife only from the husband’s account, for instance. That is not allowed. Remember the “I” in IRA stands for Individual.

However, with TSP, you cannot aggregate. You have to take the RMD straight from TSP. You cannot add the TSP’s December 31 balance to your other IRAs and then take one large distribution from an IRA. Employer sponsored plans have to be done separately. Now, we generally recommend consolidating your tax-deferred accounts to not have so many to keep track of. Consolidating accounts can simplify matters.

6. What happens if I don’t take an RMD by the deadline?

If an account owner fails to make the RMD by the due date, the amount not withdrawn is subject to a 25% penalty. (NOTE: It used to be a 50% penalty.) This can drop down to a 10% penalty if the RMD is carried out in a timely manner. (By IRS guidelines, this means “within two years.”) So, there is a penalty for not taking the correct amount by the deadline. It’s wise to work with somebody who can help you avoid these penalties.

7. Can RMDs be Roth converted–or can an RMD be rolled over into another tax-deferred account?

The answer to both of these questions is no. You cannot Roth convert your RMD. Take our example above where we calculated a $40,000 RMD for our 75-year-old. He cannot convert that $40,000. He must take a distribution, meaning the $40,000 leaves his tax-deferred account and either goes to his checking account or to a taxable account somewhere, but it has to be withdrawn. He will get a 1099 for that $40,000. If he wants to do a Roth conversion in addition to that, he can, but he cannot Roth convert that $40,000. Also, he can’t roll that $40,000 into another tax-deferred account and call that his required distribution because that would not be a taxable event. You can roll money from one IRA to another and it’s not taxable.

Most of our clients either (a) send the RMD to their checking account or direct it to another investment account (i.e., an after-tax investment account where any earnings are subject to capital gains taxes) or (b) do a qualified charitable distribution. That’s the next question…

8. Are you saying if I give my RMD away, it won’t be taxed?

Yes. This is what we just mentioned. It’s called a qualified charitable distribution (QCD). Right now the limit is $105,000 a year. That figure will be adjusted for inflation each year, and these gifts are above-the-line deductions on your tax return. That means there’s no need to itemize your deductions on your taxes.

Right now, if you give money to charity, you have to itemize to get credit for it. If you itemize your deductions and they’re not higher than whatever the standard deduction is, then you usually take the standard deduction because that’s more advantageous. In essence, you don’t get to write off the charitable gift.

What’s great about a QCD is that it is an above-the-line deduction. You get to take the standard deduction and get this QCD deduction too. Now, there is a distinction here, and it’s that a TSP will not allow you to do a qualified charitable distribution. If a QCD is something you want to do, you first have to move that TSP money to an IRA and then make the gift from your IRA.

If you’re charitably minded, this can be a great way to make your gifts even more tax-efficient. An important detail: You do have to be at least 70 1/2 years old to do a qualified charitable distribution. But if you’re already taking an RMD, you would already be above that age.

9. What options does my spouse have when it comes to inheriting your IRA?

He or she has several options.

They could take a large distribution that would be fully taxable. If the goal is minimizing taxes, then you probably don’t want to do that.

They could roll it over into their account. Or, they could open up an inherited IRA. Let’s discuss the advantages of each of these.

Let’s say that the IRA account holder had already begun taking RMDs and you (the spouse) are younger than they were and you’re not old enough to be forced to take RMDs yet. If your spouse passes and you roll the money over into your own IRA, you would not have to take RMDs because you’re not old enough yet. This move would minimize RMDs and thereby minimize taxes.

If you moved the money over to an inherited account, you would have to continue the RMDs because your spouse had already started them. In this case, to minimize RMDs, you may wish to roll the account over into your personal account.

You may be wondering what’s the benefit of opening up an inherited IRA. If you are already receiving your own RMDs, but your spouse was not, rolling that money into your own IRA would force you into taking RMDs. However, if you put that money into an inherited IRA, it would in essence delay RMDs until the year that your spouse would have turned on their RMD. If you’re trying to minimize RMDs, this is a good solution.

Another benefit of an inherited IRA is that if you are under 59 1/2 and your spouse dies and you put the money in an inherited IRA, you can access that money without a 10% penalty. Since you’re under 59 1/2, if you rolled that money into your own personal IRA–but then needed to access some of the money–you would be “underage” and therefore subject to a 10% penalty on any money you withdraw. With an inherited IRA, there is no penalty for accessing money. That could be beneficial.

A different reason to roll the money into your own IRA is if you are hoping to do Roth conversions. You can’t Roth convert the money in an inherited IRA. You can only Roth convert money in your own IRA. This may be a reason to roll the money over into your own IRA.

You might ask, “Can I move some of the money to my own IRA so I can do some Roth conversions, and move the rest into an inherited IRA so that I can access the money prior to age 59.5 if I need it?”

The answer is, “Yes. You can.” However, the rules for this are somewhat confusing; working with a professional is wise.

Postponing taxes can often be helpful, but it’s also important to know when is the best time to pay those taxes. Perhaps one year you have a higher income and you don’t want to take an RMD. In other years, you have a lower income and you would like to take it. The point is you don’t want to be forced to take money out during high-income years if you can help it. Knowing all these rules and using them to your advantage is the goal.

10. Do RMDs stop when I pass away?

If you start taking RMDs and you die, and the person inheriting your money opens an inherited IRA, there’s a 10-year rule. Your beneficiary has 10 years, starting the year after your death, to withdraw the money. Now, let’s say that to even out the tax payments, they took an even portion annually for 10 straight years. That distribution amount would still be higher than what the original RMD would’ve been.

We talked earlier about how a younger spouse does not have RMDs if they roll that money into their personal IRA to stop the RMDs.

But if a spouse or non-spouse beneficiary inherits your money and moves it into an inherited IRA, that triggers a 10-year window. In other words, the RMD’s don’t stop when you pass away. They actually get worse because the minimum amount will now be a higher percentage than what you would’ve been taking.

With so many confusing rules governing RMDs, it’s easy to mess up. You can end up paying a hefty penalty. Or, you might take RMDs–and pay more in taxes–when you really don’t need or want to. Had you simply known the rules–or been working with someone who does–you could’ve avoided some unnecessary headaches.

Don’t let that happen to you. If you’re like most people, you don’t want to be “mandatoried” into doing anything. The good news is these things can be planned out in advance to give you more freedom, and a more positive outcome.

If you’d like to watch another video on this subject, check out this one: How to Reduce RMDs in Your TSP.

Meanwhile, if you have RMD questions I didn’t address here, visit our website, christycapital.com. There–in the top right corner of the page–you’ll see a green TALK WITH AN ADVISOR button. Click it, and leave us a short message. We’ll be in touch right away.

At Christy Capital Management, we help folks take the mystery out of retirement. We’d love to help you too.