Nobody wants to stumble into retirement unprepared.

And at Christy Capital Management, we don’t want that for you. (That’s why our mission is to help our clients take the mystery out of life’s next chapter.)

Recently, I found an article listing 15 questions federal employees need to answer before retirement. It’s a thorough list.

Let’s run through it quickly. I think you’ll find it helpful.

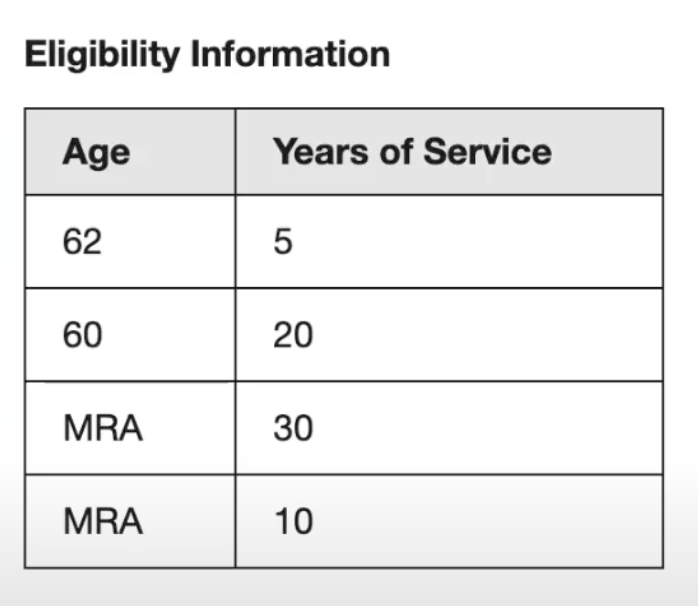

1. Do you know when you can retire without penalty?

Make sure you understand that if you retire under the MRA +10 designation, there will be a penalty. To avoid that, you need to have your MRA +30 years of service, or be 60 years old with 20 years of service, or be 62 with five years of service. These are the requirements to retire and receive the full amount right away.

2. Do you have a plan to reduce debt before retirement?

Being debt-free can help your cash flow in retirement. In this economy, however, it can sometimes be hard to pay off debt. We’ve talked to people with mortgages at, like, 3.5%. They’d like to be debt-free. But they also understand that their interest rate is so low, it might not make sense mathematically to pay them off.

At the same time, I have yet to meet the person who’s paid off their mortgage and said, “That was a terrible decision!” Debt does mortgage your future and so paying off debt is good.

However, before you take a large distribution to pay off your mortgage, do some math first.

3. Do you know the best retirement month for a federal employee?

This is going to depend on your situation. A lot of people retire in December because they’re trying to play the “annual leave game.” They store up the most annual leave they can and carry it over into their final year of working so they can retire and get a larger annual leave check.

Keep in mind that annual leave has a cash value–you’ll actually get a check in retirement? Sick leave, on the other hand, doesn’t have a cash value, it just adds to your time and your pension.

Now, I think there are some situations (for example, with air traffic controllers) where sick leave may have a cash value. but for the vast majority of people it does not. It’s just added on to your time.

For some, the best retirement month is as soon as they qualify–”When I have my 30 years, I’m retiring then!”. Generally people are retiring at the end of the month. If you want the shortest gap between retirement and your first check, then retiring closer to the end of the month is usually better.

4. Are you prepared with an emergency fund for your retirement transition?

I just spoke with a fairly new retiree. It took them eight months to get their full pension check. For eight months, instead of a check for around $3,500, they were only getting about $1,200 a month.

This individual also qualified for the special retirement supplement, but they did not get that check either for those eight months.

Of course, once the full adjudication happened, they were made whole and they got a lump sum to catch them up.

But you can see the wisdom of having an emergency fund during this transition, as it seems like OPM is taking longer and longer to process retirement paperwork.

5. Do you have updated beneficiary information, wills, and estate planning documents?

Here are the four beneficiary forms for the federal government.

- The first one is the SF-1152. This is the unpaid compensation beneficiary form. If, God forbid, you die on the job, this stipulates who will get your last paycheck.

- Then there’s the TSP-3 which is the beneficiary form for your TSP account.

- There’s the SF-2823 form which is the beneficiary for your FEGLI life insurance.

- Then there’s the SF-3102. This is a form for your survivor benefit when you retire. You won’t have filled this one out yet if you’re still working.

While we’re on the subject of beneficiary forms, make sure you have contingent beneficiaries filled out as well (in case something happens to you and the primary at the same time).

6. What is your age 62 Social Security benefit?

This is important for two reasons. One, lots of people take Social Security at 62, so it’s important to know that number.

But also, if you’re retiring prior to 62 and you’re eligible for that special retirement supplement, then you’re going to want to know what that number is. If you retire prior to 62 on an immediate annuity, then you qualify for the special retirement supplement. And so that supplement is determined based on your age 62 Social Security benefit.

7. Do you have Special Retirement Supplement eligibility?

If you retire prior to the age of 62 on an immediate annuity, then you are eligible. Now, lots of people retire at MRA which is somewhere between 56 and 57. You would be eligible to get that all the way up to 62. No matter when you retire, if you get that special retirement supplement, it will stop at age 62.

8. Do you know your creditable service years?

The important word here is creditable. This is the actual service that you’ve actually worked. To qualify for MRA +30, you’ve got to have 30 actual years. If you’re retiring at age 60, with 20 years, then your actual service needs to be 20 years.

The difference between actual and creditable involves sick leave. Sick leave does mean that you get paid a little bit more; however, sick leave can’t cause you to be eligible for retirement. You can’t work 29 and a half years, get six months of sick leave and then suddenly have your 30 years to be eligible to retire. That’s not how it works.

9. Have you kept track of your accrued leave time?

As far as sick leave goes, OPM has a sick leave conversion chart where you can figure out how much extra time is going to be added onto your pension because of sick leave.

The old saying is true: “Use it or lose it.” So, you want to keep an eye on your unused annual leave to make sure you don’t lose it. You want to get the biggest check you can at retirement.

10. Have you prepared for the interim-pay period that follows retirement?

This parallels the emergency fund question.

In theory, when you retire at the end of the month, two weeks later, you’ll get your last paycheck. Two weeks after that, you’ll get your unused annual leave check. And then, in theory, two weeks after that you start receiving your pension check.

Sometimes, however, there are hiccups in the process. And when the checks begin to arrive, they may be less than what you are expecting. It’s important to have some contingency money for this transition period.

11. Have you made your military service time deposit?

Do you have any military service time? If you do, do you want to buy it back? Generally, if you’ve got three or four years of military time, a lot of times it makes sense to buy it back.

There’s a form that you can turn in to find out what the buyback figure would be so that you can do a break even analysis to see if it’s worth paying it back.

If you’ve retired from the military and you’re receiving a pension, a lot of times it may not make sense to buy that back. If you buy it back, you will then lose the military pension and have that time count towards your first time.

I’ve only seen a couple of instances where it made sense to do that. And that’s where, for example, while in the military, the individual’s pay level was low. But then, when they got a federal job, they were at, like, a GS-15, really high pay scale. That’s rare.

So, most of the time buying back military time–if you’ve already retired–may not make sense. Buying back three or four years of military time probably does make sense. We always want to do the math on situations like that. That’s something that we help clients with.

12. How is your TSP account balance distributed between the various funds?

They’ve recently opened up more L-funds with 5-year increments as opposed to 10 years. They’ve also opened up the mutual fund window with a whole ton of choices.

I think the question to ask is “How aggressive or conservative are you set up?” And maybe I should ask, “How diversified are you tax wise? How much of your money is in traditional accounts and how much is in Roth?”

It’s important to understand who you are as a person–and as an investor. How aggressive do you want to be? It’s crucial to have your TSP balance align with your “risk temperament.”. If you need help with how your investments should be set up, our team at Christy Capital would be glad to help.

13. Do you have the right coverage for Federal Employee Group Life Insurance (FEGLI) and long-term care planning?

Generally speaking, FEGLI is quite cheap when you first start out as a young worker. As you get older, it starts to get more and more expensive. We’ve done videos detailing when it gets expensive enough that you may want to look for other coverage.

What about long-term care planning using the federal government’s long-term care Insurance? In December of 2022, they put this program on hold for two years. New people cannot sign up for this coverage.

However, both FEGLI and long-term care can be covered in the private sector by using life insurance.

Some are replacing FEGLI with term life insurance. It has a set price that will never change for the life of the term. That could be an improvement over FEGLI, as FEGLI gets more expensive every five years.

In some instances, we also use life insurance to replace long-term care insurance policies. You can get a permanent life insurance policy which means that the death benefit will be payable no matter when you die. You can die at age 95, and it will still pay.

But the death benefit also doubles as long-term care insurance. Let’s say you’re 80, and you need long term care and you qualify for it. You have the option of either spending your money and leaving the death benefit intact for your beneficiary. Or you can dip into the death benefit and spend that for long-term care and leave your other money alone.

There are two issues with FEGLI as I see it: It gets more expensive all the time; and it doesn’t currently offer long-term care. Again, life insurance can be a viable option. To learn more about these options, reach out to us at Christy Capital (866) 331-7749.

14. Do you understand how your unused annual leave is considered at separation?

Remember, unused annual leave has cash value. They take your hourly rate at retirement and they multiply it by the number of hours of unused annual leave, and you get a big fat check–hopefully.

But guess what comes with that big fat check? Big fat taxes!

It’s crucial to factor that into your planning.

15. Have you been enrolled in FEHB at least five years before retirement?

One of the great benefits of being a federal retiree is that you get to take your health care into retirement with you. The government pays 72%–just like they do when you’re working. And they will continue to pay it when you retire.

The issue is: You have to have been enrolled in FEHP for five years. If you’re a spouse of another federal employee, then as long as you’re on the family plan, or the single plan for five years, you’re covered. If you’re military and you’ve had TRICARE, that also counts towards those five years. Every once in a while we’ll run into somebody where they just recently got FEHB and now they realize they gotta keep working to get the five years in.

One last thing…

And if you have:

- $400,000 or more in your TSP

- And you want help planning your retirement