You’d be surprised at how many people think retirement readiness involves just two factors:

- how old you are

- how much you’ve amassed in your portfolio

It’s a bit more complicated than that.

We know this because, since 2005, our team at Christy Capital has worked with thousands of federal employees, helping them prepare for life’s “next chapter.”

In guiding so many people through the often-confusing landscape of retirement planning, we’ve identified five questions you need to ask and answer so you can prepare for retirement.

The first question is…

1. What does an ideal retirement lifestyle look like for you?

Will you be moving to a new state? Are you hoping to do charitable work? Do you plan to travel? What kind of lifestyle do you envision in retirement—and how much money will you need monthly to fund that lifestyle?

Many assume their expenses will stay the same throughout retirement. However, what we’ve found is that retirees often go through three distinct phases.

In the early years of retirement, people tend to be more active. We call those the “go-go” years. This is when retirees are prone to travel and spend more.

Next, many often go through a period where they don’t spend as much money. We call those the “slow-go” years.

For many, there comes a third phase when medical issues arise—and medical expenses rise too. Suddenly, there’s not as much traveling. We call that period the “no-go” years.

In short, your lifestyle expenses in retirement won’t be linear. That’s the key takeaway. Your spending will likely go up and down.

Here’s a second question to ponder:

2. Which retirement accounts are you going to reach into first to take money from?

For a lot of people, a traditional TSP or IRA is the only retirement asset they have. If that’s the case, this question is pretty easy. You’re going to supplement your pension and/or Social Security income with money from your traditional assets.

But hopefully, you’ve been watching our videos. As a result, you see the importance of diversification. Like most people, you want to have some traditional TSP or IRA money. But you also realize it’s smart to have some Roth money that will come to you tax-free.

Ideally, you’d also have some taxable money that you could get your hands on with no age restrictions or limitations. We call that non-qualified money, and it’s ideal for emergency situations.

Here’s what happens when our clients call up needing money. We go through a list of their assets that we’re managing, and we look at which account makes sense to withdraw the money from.

If we take the needed cash from a non-qualified or a joint account, that’s not retirement money. They may have to pay capital gain taxes on the growth. Of course, that all depends on what’s been going on with the market. If they don’t have any gains on which to pay taxes, that might be a good place to tap if they need money.

However, if you have such an account—and you’ve had it for a number of years—you probably have some gains there. Because of that, you may not wish to withdraw money from that account.

Since there are multiple factors to consider, it’s smart to have someone walk you through your options. (It can also alleviate your stress.) Remember: If you take money from a traditional TSP or traditional IRA, the entire distribution will be taxable.

Now, if you have a Roth account that’s at least five years’ old, and you’re over age 59 and a half, you may take the money from that account, and it could be tax free. At first glance, that may seem the logical place to get your money from.

But let’s look at it a different way. It took a lot of effort to get that money in your Roth account. And assuming it grows over time, it grows tax-free. For that reason, you might not want to withdraw money from your Roth account. In fact, that Roth money may be the last money you ever want to touch. Again, it depends on your unique situation.

Ideally, you want to have multiple options. Depending on your situation and what’s going on in your life at the time, it may make one account the obvious winner of where you should take the money from. But it does require some planning and thought.

What we find a lot of times is that people really don’t have a choice in what bucket or which account to pull from. They only have one account—their traditional TSP or IRA. And so when they do need that money, it’s taxable.

Here’s a third question to ask…

3. When will you take Social Security?

In reality, there are endless options, but we typically talk about three primary choices:

- Do we start taking Social Security at age 62?

- Do we wait until full retirement age (i.e., 67)?

- Do we wait and turn on Social Security at age 70?

Age 62 is the earliest you can start collecting Social Security payments. But be warned: If you were born in 1960 or later, and you turn it on at age 62, you’re only going to get about 70% of your full retirement age benefit.

Full retirement age is 67. That’s when you get 100% of the benefit that you’re supposed to get.

The last scenario is waiting until age 70. If you do that, you’ll actually receive 124% of what you would have gotten at your full retirement age of 67.

Again, these three choices aren’t the only possibilities; there are other options available with Social Security. Every month you delay, you’ll get a little bit more money. So, you can turn it on at age 63 and three months if you want to. Or age 64 and five months. You get the idea.

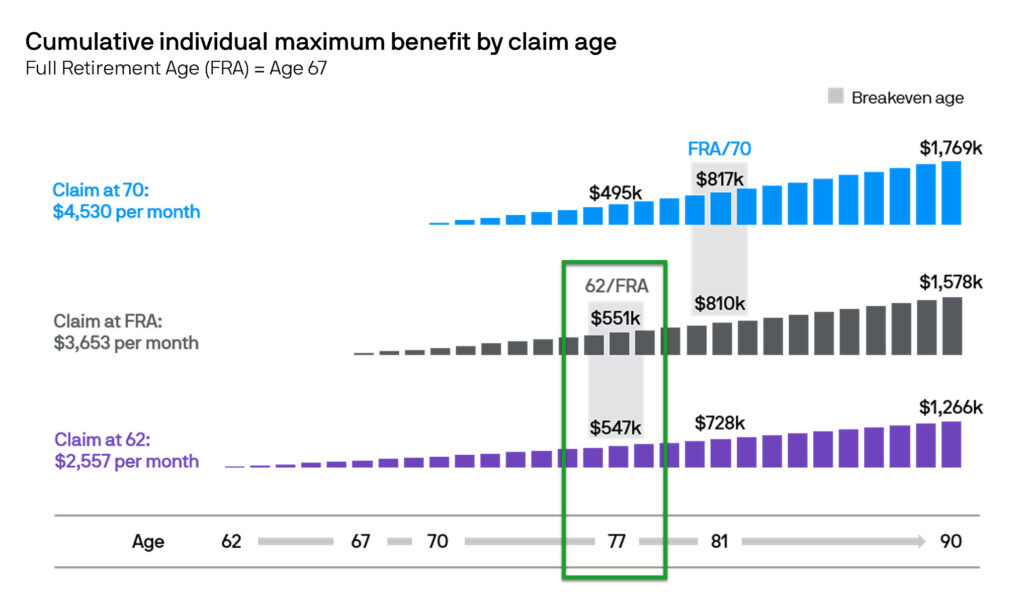

Following the question of “when,” the discussion usually turns to “How?” How can I maximize it? Where’s the break-even point?” This depends on how long you think you’re going to live.

A recent study from JP Morgan compared turning on Social Security at age 62 versus waiting until full retirement age. You can see that 77-years-old is the break-even point.

In other words, if you think you might live longer than age 77, you’re better waiting until age 67 to take Social Security. However, if you’re not expecting to live to age 77, it’s better to turn it on prior to full retirement age. Age 62 would be the better move in that scenario.

The break-even point between turning it on at full retirement (age 67) versus age 70 is 81. That means if you think you’ll live longer than age 81, you’re better off waiting until age 70 to start collecting Social Security. That will give you more money in the long run.

The problem with all this speculation, of course, is that none of us knows how long we’re going to live. But, perhaps based on your family’s health history, you have an idea and you can use this guesstimate in your planning.

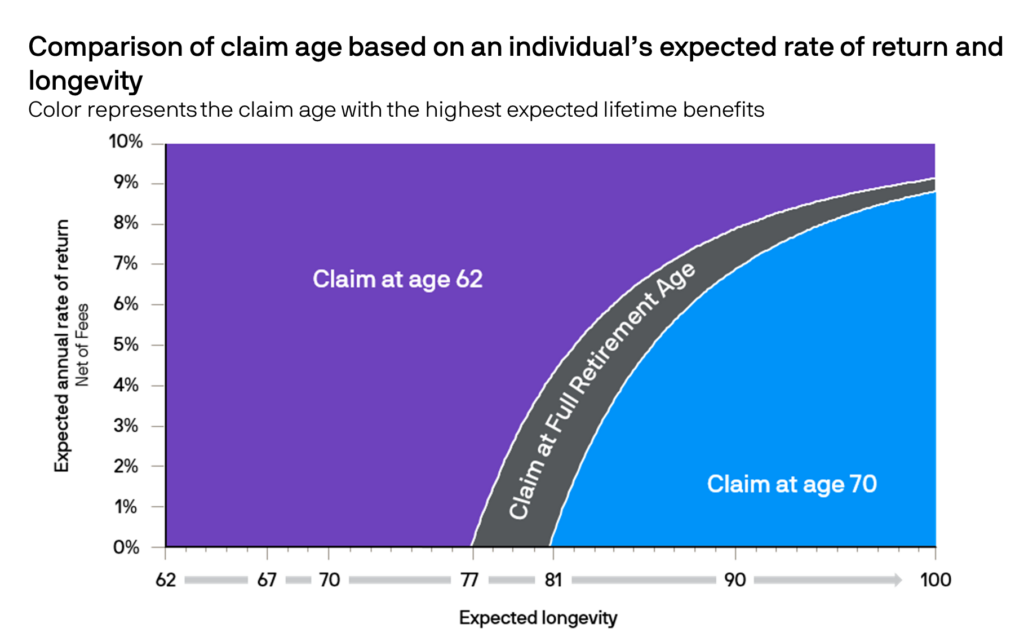

Now, suppose you turn on Social Security early. But rather than spend that money, let’s say you invest it. Could you end up with more than you could get by waiting for a larger Social Security check at age 70? That depends on what kind of return you’re able to get on that invested money.

This chart from JP Morgan may prove helpful.

Let’s say you live to be 82, but you only earn 1% on your money. In that case, waiting until age 70 is better. But suppose you lived to age 81, and were able to earn 8% on your money. In that scenario, the better option would be to turn on Social Security at age 62.

If you are a more aggressive investor, and confidently expect a higher rate of return, it may make sense for you to begin receiving payments early so you can reinvest those Social Security payments.

Here’s another question to consider…

4. How will you pay for health care?

One of the great benefits of being a federal retiree is that you get to maintain your federal employee health benefit (FEHB) in retirement as long as you had it for five years prior to retiring. In that program, the government pays 72% of your premiums and you pay 28% of the premiums.

No private sector companies pay 72% of the health insurance premiums for their former employees. So, federal retirees have a great thing going.

In retirement, the federal government will pay the same portion with one major difference: You have to pay your premiums with after-tax dollars once you retire (as opposed to before-tax dollars while you were working). Other than this, your federal health care will act the same way in retirement that it did while you were working. Same co-pay, same everything.

At age 65, Medicare then comes into play. We’ve created some specific videos that discuss whether you should do FEHB with Medicare or FEHB on its own. Feel free to check those out here. And take comfort in this fact: Because you have federal healthcare, this will not be as much of a worry as it would be for a non-federal retiree.

5. How will you fund your retirement?

If you’re a federal retiree, you’re going to have a pension. You’ll have Social Security and—if you’re married—spousal Social Security. You’ll have your traditional TSP or IRA and/or a Roth TSP or IRA—if you set such things up.

Some people purchase annuities. That’s another option to diversify.

The bottom-line? Federal retirees and their pensions allow them to fund retirement in a better way than most non-federal workers.

Whatever your situation, creating a financial blueprint can show you the income you’ll have coming in versus the expenses you’ll be paying out. That vital tool helps answer the question: Do you have enough money for retirement?

If you could use some help planning for retirement and you want to talk with someone who understands all the ins and outs of federal benefits. In the upper right-hand corner, click that green button that says “TALK WITH AN ADVISOR.” It’ll take you to a form where you can leave us a short message. We’ll get back to you promptly.

One last thing: If you’re close to retirement and wondering Am I too late to start a Roth TSP? check this video out right here. It will likely answer any questions you have.