Say the phrase “risk in retirement,” and most people will fixate about one thing and one thing only: stock market risk. That is the main concern they have, the scenario they fret about most.

Mostly they’re thinking I can’t afford a bear market to adversely affect the value of my retirement assets.

In this blog post and video, we’re going to review that risk—and six other retirement risks that, left unaddressed, have the potential to derail your retirement plans.

1. Stock market risk

Let’s start with that dominant fear I just mentioned…

The fancy term is systematic or unsystematic risk. Basically, the concern here is that if you keep most of your investments in stocks, and the market plummets, you’re going to lose money.

To mitigate against this, many people make allocation changes. They take some “aggressive money” and move it to safer investments.

But remember: Every decision has unintended consequences.

For example, when you move your money from stocks to, say, bonds, you introduce interest rate risk, inflation risk, and longevity risk (we’ll talk more about all these risks in a moment). So, it’s important to think through any such moves.

2. Tax rate risk

A second retirement risk is…

Let’s say you have a traditional IRA (Individual Retirement Account) or TSP (Thrift Savings Plan). And let’s assume you’re in a 20% federal income tax bracket—with another 5% going to state taxes. That means only 75% of your traditional balance is yours—the other 25% is earmarked for taxes. (Remember, the money in traditional retirement accounts is tax-deferred.)

So, what is tax rate risk? It’s the risk that tax rates could rise and negatively affect you.

Perhaps an illustration will help. Let’s say you’ve got a $1,000,000 balance in your traditional IRA and/or TSP. In actuality, because of taxes, that means $800,000 is “your money,” and the other $200,000 is money you’re holding for the government.

But suppose taxes creep (or jump!) up to 35% (federal + state). Suddenly, you only have $650,000 for retirement. You just lost $150,000 because the tax rates changed!

Is that a real risk? You bet it is. If you retire at 60 and live to age 95, that’s 35 years. Think there’s a chance tax rates may climb over a third of a century?

Nobody can say for sure. But most people I talk with assume taxes aren’t going to get lower.

So, how could you address this risk?

One way is to move some of your traditional money over into a Roth account now. In other words, go ahead and pay taxes on that money now, at a tax rate you like, so you won’t be affected later if taxes increase.

This common practice is called a Roth conversion. A traditional TSP won’t let you do this, but your traditional IRA will. So, if you’re old enough—at least 59 and a half and over, whether working or retired—you can move money out of your traditional TSP into a traditional IRA…and then into a Roth IRA. We do that all the time for our Christy Capital clients.

A third retirement risk is called…

3. Longevity risk

This is the risk that you end up lasting longer than your money does. You outlive your money.

There are several ways to fix this. An obvious one is to earn more money and set it aside.

Another option is to purchase a guaranteed annuity. This is where you give an insurance company some of your assets and, in return, they promise you guaranteed payments for the rest of your life.

Maybe you have a federal pension with a cost-of-living adjustment built into it—and it’s guaranteed for life. Most retirees receive a lifelong Social Security payment that has the same cost-of-living feature.

But longevity risk is an issue—if you don’t earn enough and/or your money doesn’t grow enough.

A fourth risk is…

4. Interest rate risk

This is the risk that a change in interest rates can cause you to lose money.

Think back to the 2008 housing crisis. When the stock market crashed, a lot of people moved money to bonds to get out of the stock market. Interest rates were relatively high, but the Federal Reserve kept lowering them which was great for bonds. They did amazing.

But think about where we were in 2022. Interest rates were pretty low. When the Fed started raising rates it was bad for people holding bonds. In fact, the F Fund was negative—something that hasn’t happened since 2013.

Generally speaking, bonds don’t perform well when interest rates go up because of interest rate risk. So, the people who got out of the market—moving to bonds—to avoid stock market risk inadvertently introduced interest rate risk to their portfolios. They traded one problem for another!

There are conservative options that don’t involve interest rate risk—but that’s where you need to talk with somebody that understands these risks.

A fifth risk is…

5. Mortality risk

This is the risk of dying early. Working with clients at Christy Capital, we always look at the scenario of “What if one spouse, let’s say the husband, dies early? Will his widow have enough money to live into her 90s? If not, how can we fix that?”

One of the things we look at in our planning is the total amount of money you have. Because that’s a sure way to offset mortality risk—simply have more money. Another way is to grow more money—to perhaps be more aggressive in your investing.

Some people realize If I were to die early, my spouse wouldn’t have enough money. So, they purchase life insurance.

It could be that your pension has survivor benefit options. That’s another option for income.

You need to keep all these things in mind.

Here, you can see the value of a good financial plan—and planner. He/she can troubleshoot various scenarios. The goal is to make sure that the remaining spouse has enough to offset the mortality risk.

A sixth retirement risk is…

6. Inflation risk

This is simply the risk (more like “reality”) of increasing prices. As time passes, we have to pay more because things cost more.

Here, the risk is running out of money because inflation slowly erodes your purchasing power. You have to pay more of your money to get the same things. The value of a dollar keeps shrinking.

This is why it’s necessary to look at inflation adjusted returns.

In 2021, federal employees with the G fund in their TSPs earned around 1.4 percent. That’s not keeping up with inflation. In fact, that’s a negative inflation adjusted return.

One way to fix this is to get better returns—at least even with or, ideally, above and beyond the current inflation rate. Anything less and the longevity risk comes back—i.e., the prospect of outliving your money.

I mentioned some retirees opt for a guaranteed payout annuity. You turn over some money, and let’s say they give you $1,000 a month for life. That sounds good, but 20 years from now, that payment will still be $1,000 a month. If inflation has crept up, $1,000 won’t be spent like it does today. In other words, fixing longevity risk with an annuity—a guaranteed payout monthly check—increases the possibility of inflation risk.

Every decision has a consequence. To put a sound retirement plan together, you need to see how all these are interconnected.

The final risk I’ll mention is…

7. Sequence-of-returns risk

We all know that negative returns are inevitable at some point. However, it makes a big difference when they come. Let’s look at an example when you’re adding, say $10,000 a year, every year, to your retirement savings.

At the end of the five years in scenario A you’ll have $159,000. That’s an average return of 7.6%. Now, look at scenario B. You’re going to have about $182,000, an average return of over 10%.

Why the difference?

It’s because of the sequence of returns. When you’re adding money, it’s better to have negative returns early. You’re buying those investments low. That means there’s more there to grow and produce good returns later.

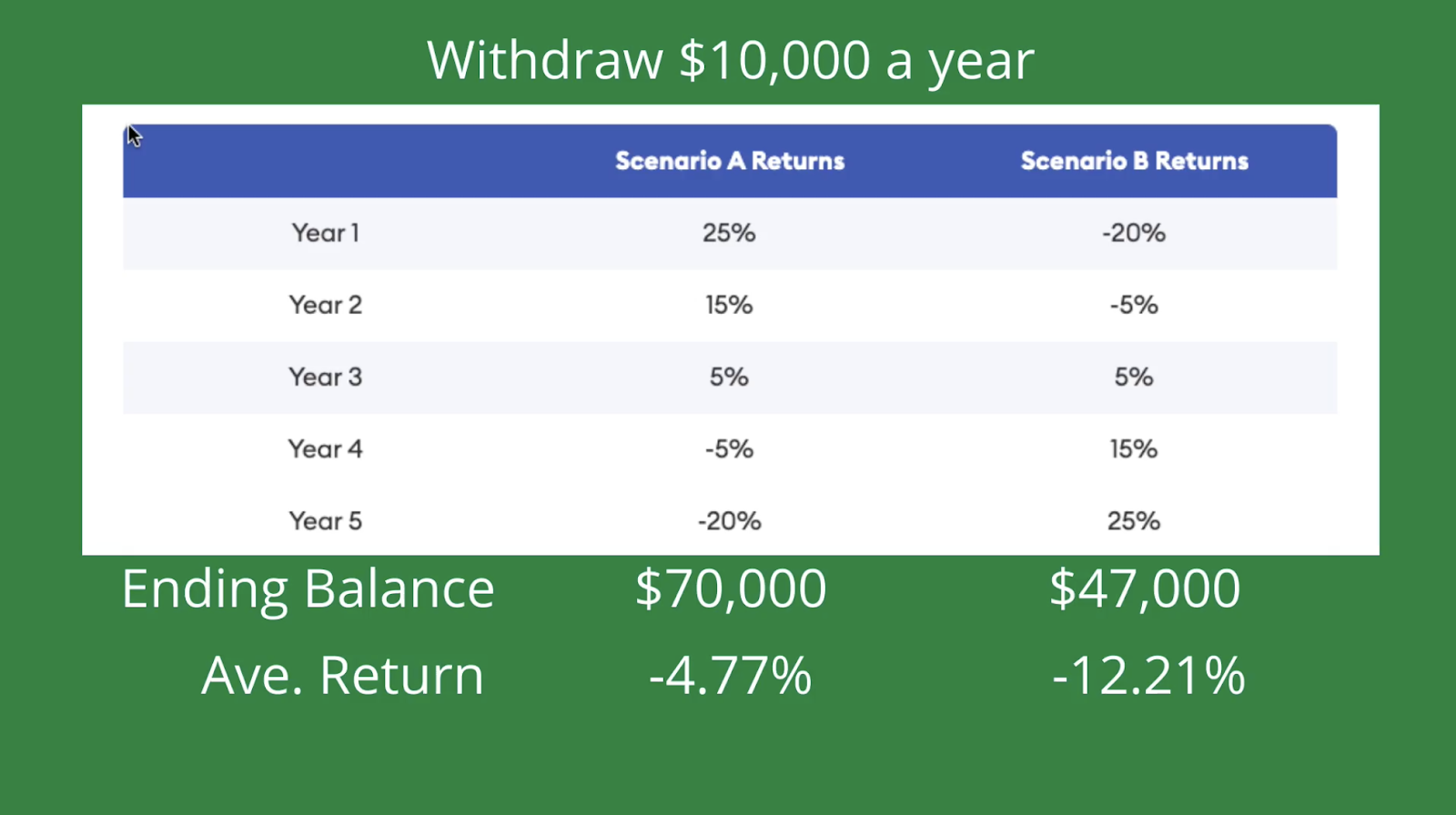

What about when you’re taking money out?

In this example, you’re withdrawing $10,000 a year. Everything else is the same. Scenario A shows, after five years, a $70,000 balance, which means your average return is a negative 4.7.

In scenario B, you’d only have $47,000—and be averaging a negative 12% return. What’s up with that? When the negative years come early and you’re taking money out, there ends up being less there to rebound in the better, later years.

Sequence of returns is huge if you have several bad years in a row. Case in point? The 2000-2001 dotcom crash. Then, the stock market had three negative years in a row. The people who had just retired and were taking money out of their retirement accounts, saw their balances dwindle quickly.

This is another reality that needs to be accounted for—especially if you’re doing your own retirement planning. Fail to factor in any of these risks, and that oversight can come back to bite you on the backside.

If you have questions about any of this or would like to discuss strategies for minimizing your retirement risks, we’d love to help. Go to christycapital.com. In the upper right-hand corner, click the green button that says “TALK WITH AN ADVISOR.” We’ll be in touch right away!