Talk about a cruel example of adding insult to injury…

Your spouse dies. A few months later, while you’re still reeling from grief, your CPA informs you that because of your partner’s death, you’ll now have to start paying 25% more in taxes!

Thankfully, it doesn’t have to be this way.

“Death Taxes”

When people bring up the “death tax,” they usually mean estate taxes. Truth be told, most folks don’t have to worry about estate taxes affecting them. That’s because the current federal estate tax exemption is $13.6 million. As long as your estate is worth less than that figure, you don’t owe any estate taxes. (Note: This exemption amount is scheduled to drop roughly by half on January 1, 2026–unless Congress renews the Trump tax cuts of 2017 before the end of 2025.)

Here’s the question: Is there any other sort of “death tax” that can cause you to pay higher taxes? I believe there is, and that’s the focus of this column.

The Death Tax Most People Overlook

Let’s say you’re married and you file taxes using the married filing jointly tax bracket. Then you or your partner dies. The surviving spouse immediately gets bumped down to the single tax bracket.

The top of the 22% bracket in 2024 for married filing jointly is $201,050 of taxable income. The single tax bracket at the top of the 22% is half that–$100,525. In fact, the lower five tax brackets for those filing single are half of what the married, filing jointly is. (The top two brackets are set up a little differently and are not halved.)

A fictional case study shows how this would affect a new widow or widower.

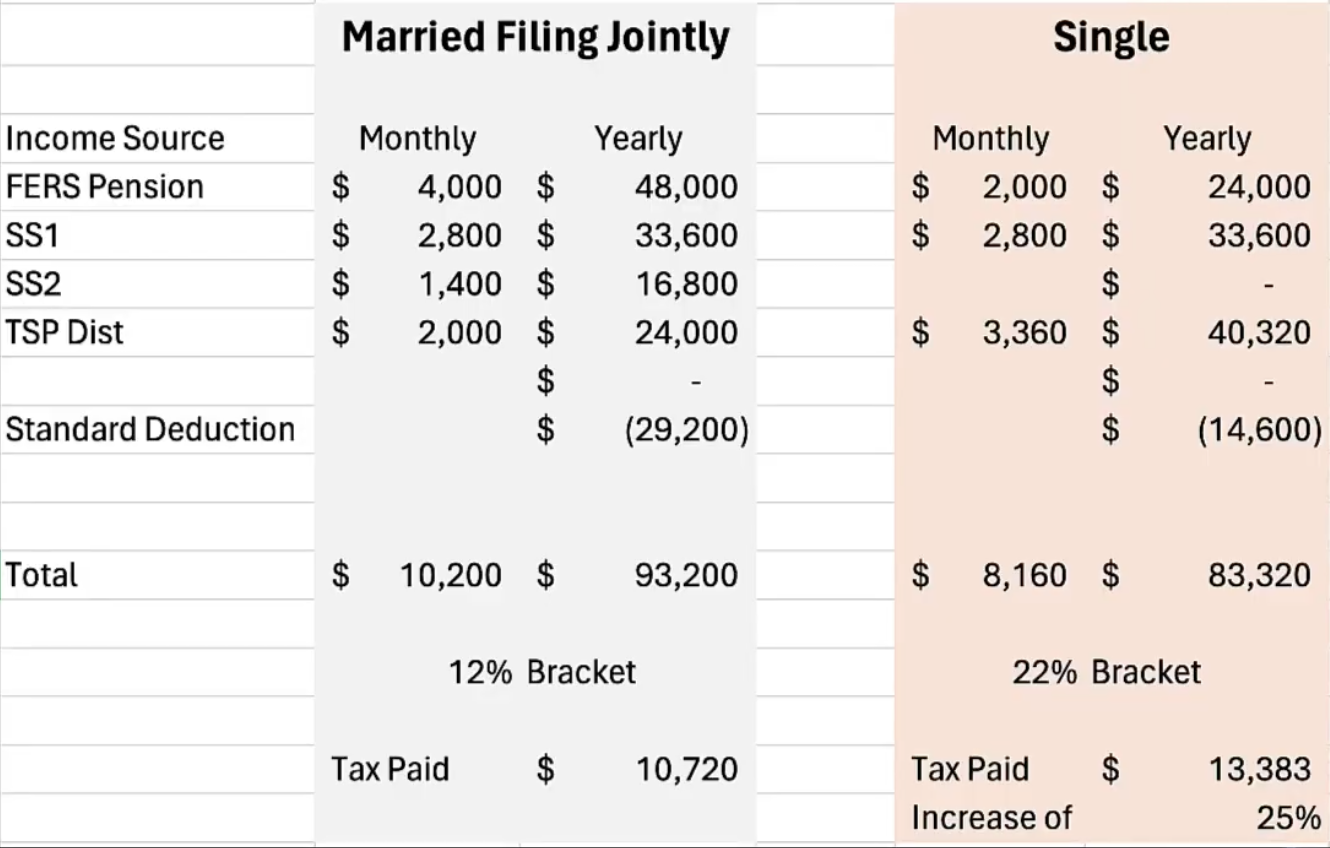

Let’s say an individual retires and has a $4,000 FERS pension. They also get $2,800 monthly from Social Security, added to the $1,400 their spouse receives monthly from Social Security. Let’s further assume this couple takes a $ 2,000-a-month distribution from their traditional TSP. This gives them a total monthly income of $10,200 a month. Now, let’s do a little simple tax return.

Note: This is a simplified example only to illustrate the tax benefits of careful planning. Always seek out professional help with your taxes and tax returns.

So, here we have the annual totals of a $48,000 pension, $33,600 in Social Security for one spouse, $16,800 in Social Security for the other spouse, plus $24,000 as a yearly distribution.

To keep our illustration simple, let’s subtract the standard deduction. That gives our fictional couple an annual income of $93,200. Using the married filing jointly tax brackets, our couple barely squeaks into the 12% tax bracket.

The Overlooked “Death Tax” Rears Its Head

Now, let’s say tragedy strikes. One of the spouses dies. When we apply the 50% survivor benefit, that $4,000 pension suddenly drops to $2,000 monthly. The larger Social Security benefit of $2,800 a month remains in place and the $1,400 smaller Social Security payment disappears.

We typically estimate that a single person’s expenses are about 80% of what a married couple spends. So, instead of needing an income of $10,200 a month, that figure drops to $8,160 monthly. However, this means the surviving spouse will need to take a larger, $3,360 monthly TSP distribution.

Using the standard deduction, this gives a taxable income of $83,320. According to the single tax bracket, our grieving widow/widower is now in the middle of the 22% bracket!

While married, they were in the 12% bracket. Following the death of their spouse, this individual was suddenly moved to the 22% bracket. What does this mean in actual dollars? A 12% tax rate* for the couple with $93,200 in income resulted in them owing $10,720 in taxes (*Remember, not all income is taxed at 12%. Some is taxed at 10%. Again, this is an oversimplified example for illustrative purposes only.)

However, our bereaved single person is now paying a 22% tax rate on a lesser income of $83,320. This translates to a tax bill of $13,383. That’s a 25% jump in taxes solely because a spouse died.

This is where percentages alone can be misleading. Indeed, going from the 12% tax bracket to the 22% bracket is a 10% increase in tax rate. However, going from $10,720 to $13,383 in taxes is a 25% jump in actual dollars!

Let’s take this a step further. By owing an additional $2,600 a year in taxes, our widow/widower will have to withdraw an extra $2,600 a year in distributions to remain at the same income level.

That additional $2,600 a year could translate into running out of money faster. Depending on other factors, it may jeopardize the retirement plan that’s in place. And why did all this happen? Simply because a spouse died. That sure sounds like a death tax to me. Can this scenario be avoided?

Avoiding the “Death Tax”

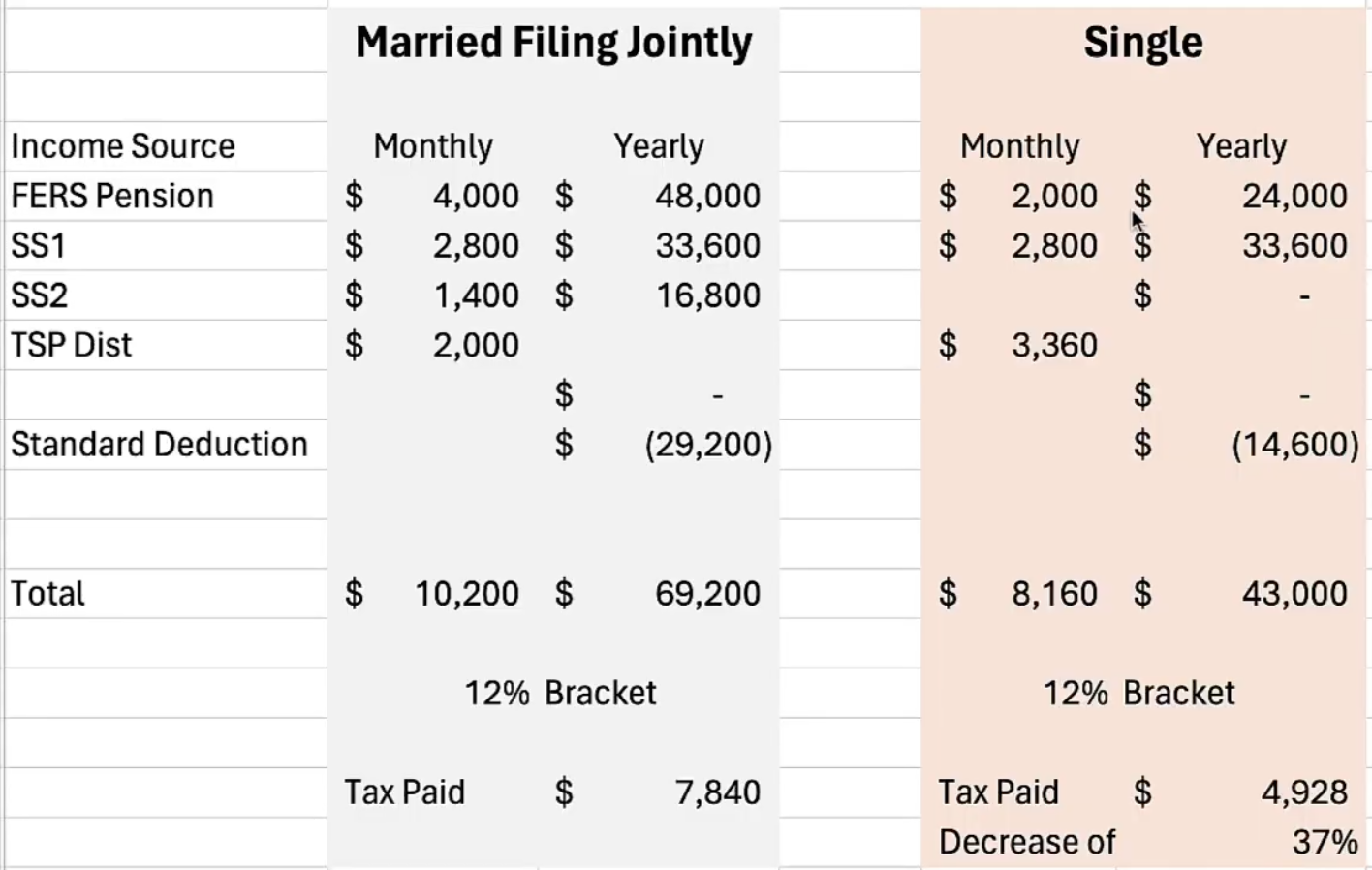

The good news? It is possible to avoid this kind of Widow/Widower Tax Trap.” Let’s look at the numbers. Let’s say our couple had instituted a proactive tax planning strategy where, over time, they shifted money from their traditional TSA to Roth. Once they did that, all their retirement assets were in Roth. When they began taking out distributions, they owed no taxes on those withdrawals.

Under this Roth scenario, our fictional couple would have the same income: a $4,000 a month pension, $4,200 total in Social Security income ($2,800 + $1,400), and $2,000 a month from their assets. But, again, since that money was coming out of their Roth account, it would not be taxable.

Applying the standard deduction, our couple would have a total income of $69,200–which is still in the 12% bracket.

When one of the spouses dies, the survivor would move to the single tax bracket. He/she would receive a $2,000 monthly pension, $2,800 a month from Social Security, and a $3,360 monthly distribution from his/her assets (to account for the drop in pension and SS income). Again, however, that money would be coming from a Roth account. It would not be taxable.

Filing single and applying the standard $14,600 deduction, this individual’s taxable income would come to just $43,000. According to the single tax bracket, that put this person in the 12% bracket.

So, not only would there be no increase in taxes, there’d be a 37% drop in the amount of taxes owed even though–cash flow-wise–the person would be living on the same monthly income and maintaining the same standard of living. How? Why did this happen?

It happened because of proactive tax planning. Money was shifted from the taxable traditional TSP (or IRA) to a non-taxable Roth account. Remember, you can’t do this kind of planning inside a TSP. You first have to move the TSP money into a traditional IRA. From there, you can move it into a Roth account.

If you’re concerned about this sort of “death tax” creating problems for you in retirement, we’d love to help. This is something we do for clients all the time.

Or, maybe you’re wondering “From which account should I withdraw money first when I retire?” If so, check out this video Should you Withdraw from Traditional or Roth First in Retirement? That’s a smart question to ask since different accounts are treated differently from a tax perspective.

Meanwhile, if you have other questions about retirement planning, visit our website, christycapital.com. There–in the top right corner of the page–you’ll see a green TALK WITH AN ADVISOR button. Click it, and leave us a short message. We’ll be in touch right away.

At Christy Capital Management, we help clients take the mystery out of retirement. We’d be honored to help you too.