Craig is confused. His brother is urging him to invest systematically:

“Just have $150 automatically deducted from each paycheck and put into your TSP. Over time, I promise, you’ll reap the benefits of dollar-cost averaging and compounding.”

Meanwhile, Craig’s best friend—who recently became a day trader—is trying to sell him on the strategy of “buying the dip.”

What do these phrases even mean? And which strategy is best for Craig? Most importantly, which one is best for YOU?

That’s the focus of this post (and companion video).

First, let’s define our terms for these investment strategies.

Two very different strategies

“Buying the dip” refers to the strategy of purchasing an asset—typically shares of stock—when the asset experiences a decline. The hope is that it will rebound and yield even higher returns. Some people refer to this practice as “timing the market.” This style of investing is more opportunistic and sporadic.

“Dollar-cost-averaging” is a financial practice whereby a person regularly invests a fixed amount of money at scheduled intervals, regardless of the stock market’s current performance. The goal is to reduce the impact of market volatility on the overall cost of the investment over time. This kind of investing is more habitual.

What the research shows

Nick Maggiulli, Chief Operating Officer for Ritholtz Wealth Management LLC, has written an intriguing article entitled “Even God Couldn’t Beat Dollar-Cost Averaging.” It’s a bold title (and a provocative claim). But is it true?

Mr. Maggiulli did extensive research on which investment approach—buying the dip or dollar-cost averaging—performed better over a 40-year period. What he found may shock you.

Imagine living between 1928 and 1979. And you want to invest in the U.S. stock market for 40 years. You have two strategies that you can choose from.

One is “dollar-cost averaging” where you invest, say, $100 per month, no matter how the market is doing, and you do this consistently for 40 years.

Your second option is trying to “buy the dip.” That is, you set aside the same $100 a month, but you only buy into the market when there’s a dip. What do we mean by a dip? A dip is defined as any time the market is not at an all-time high.

For fun, I’m going to make this “buy the dip” strategy even more attractive. Not only will you buy the dip, but we’re going to make it so that you as the investor are omniscient (i.e., “all-knowing”)! In other words, you’ll always know exactly when the market hits an absolute bottom between two all-time highs.

So, imagine the stock market going up and reaching an all-time high. It eventually goes down, then climbs to a new all-time high. Because you’re “all-knowing,” you’re able to invest at the lowest point between those two highs. This ensures that you’re buying that stock at the lowest possible price.

The only other rule for this experiment is that you are not allowed to move in and out of different stocks. Whichever strategy you use, once you buy, you have to hold those investments for the entire time.

Now…given these parameters, which strategy do you think would result in the bigger gain? We tend to think that knowing the dip—and buying only at that time, between two peaks—has got to be the fool-proof strategy. But what does the data show?

It shows that buying the dip underperforms dollar-cost averaging 70% of the time! This is true even though you knew exactly when the market was at the bottom between two all-time highs.

Why is this true? Buying the dip only works if you know that you’ve reached the bottom of a decline, and you can time it perfectly. What’s more, severe dips—where you stand to get huge returns—are rare events. Therefore, the strategy rarely beats dollar-cost averaging.

And if we took away your omniscience (and thus, your perfect timing) so that you were no longer buying exactly at the dip…and if we moved you by two months—that is, you either bought two months before the dip or two months after the dip (which is truer to how investing usually works in real life), then dollar-cost averaging goes from winning 70% of the time to winning 97% of the time!

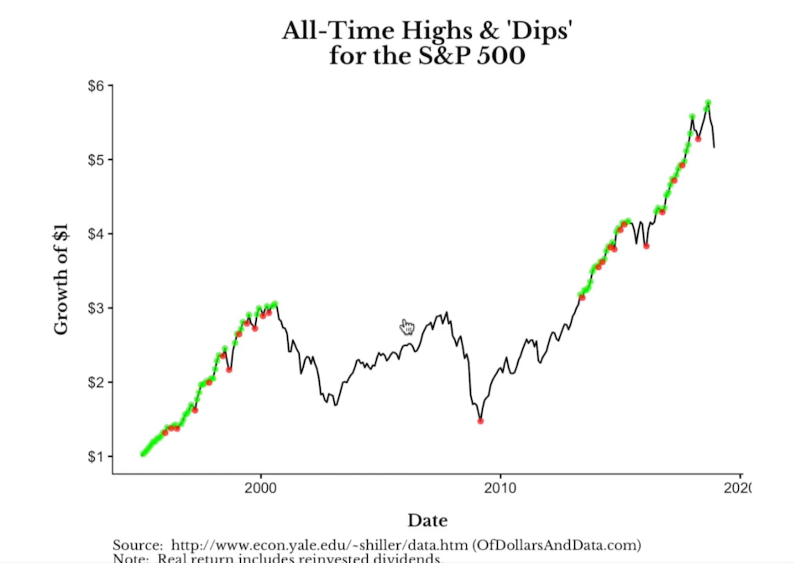

Examining the Data

Look at a chart spanning from January 1995 to December 2018. All the green dots are the all-time highs. Buying the dips would be any of the lowest points between those green dots. You can see we have red dots to represent each omniscient buying of the dip.

The dip that stands out is the March 2009 dip. The others, as you can see, are less significant.

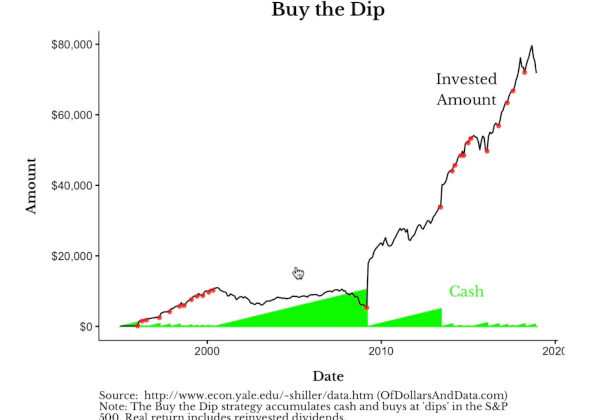

Here’s a chart that shows how buying the dip would work.

You can see, around 2000 or so, the last red dot at which you would have bought the dip. Then as the market goes (mostly) down to March 2009, you can see (indicated by the green) how much money you would’ve accumulated to make your next “dip purchase.”

Then, as the market rises, you can see along the bottom, the green getting bigger. That’s because, again, you’re saving money until it’s time to make your next “dip purchase,” which will happen around 2013.

One reason that dollar-cost averaging wins as a strategy is that the earlier you invest, the earlier your investments can compound and grow.

The fact is, there are only a handful of big dips like March of 2009. When you can take advantage of those, it’s fantastic. However, the time you spend waiting for dips is time your money is missing out on the power of compounding interest.

For these reasons buying the dip only works well when you do it early on. When you look at longer timeframes, you can see that, historically speaking, buying the dip rarely outperforms dollar-cost averaging.

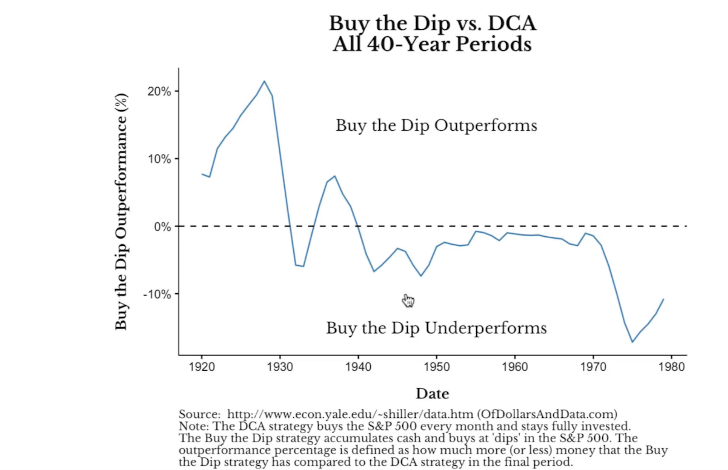

Here’s a chart that shows when buying the dip worked well between 1920 and 1980—and when buying the dip underperformed.

In the 1920s (also known as the “Roaring Twenties”) the buy-the-dip strategy was profitable. Then came the great Stock Market Crash of 1929, which resulted in another opportune time to buy the dip. Overall, the strategy worked fabulously until about 1940.

Since that time, you can see that buying the dip has underperformed. Dollar-cost averaging has been the winning strategy.

What does all this mean for you?

The big takeaway of Mr. Maggiulli’s research is that if you attempt to build up cash so you can buy into the market at the next big dip, odds are you will end up worse off than if you had just invested that money every month. While you’re waiting for the next dip, the market is likely to keep rising, leaving you behind.

And remember, if you mistime guessing the bottom—even by two months—it drops your chances of success from 30% to just 3%! (And you are likely to mistime it because none of us is omniscient.)

For most people, these findings are going to be welcome news. You are investing money into your TSP systematically every pay period.

But as you enter retirement, you won’t be contributing any longer. At that time, you’re going to want to make sure you have an allocation of investments that matches your risk tolerance level. If that’s a concern for you, check out this video right here [need link].

Why is your TSP invested like it is? What strategy are you using? If you want more information about that, watch this video right here [need link].

And if you have $400,000 or more in your TSP…but don’t yet have a financial advisor to help you with financial questions like this, our team at Christy Capital would love to help.

Click here and leave us your contact information. We’ll get in touch right away.

At Christy Capital, our mission is to help you take the mystery out of retirement.