In finance, the Rule of 4% is a well-known concept. It’s been tested and proven to aid individuals in planning for retirement.

What is this rule (and who made it)?

This 4% Rule originated back in 1994 from a paper published by a financial advisor named William Bengen. He was trying to answer the question: “What is the ideal withdrawal rate from one’s retirement investment portfolio?”

Others took his research and experimented with a wide range of withdrawal percentages ranging from 3% up to 12% and with various portfolios, offering various mixes of stocks and bonds. In each case, a 30-year time horizon was used.

Using a 50-50 stock-to-bond ratio, it was determined that withdrawing 4% annually would leave a person’s portfolio intact 30 years later, 96% of the time.

So, for example, if you had a $1,000,000 portfolio, with 50% invested in stocks (let’s say the C-fund) and 50% in bonds (let’s say the G- or F-fund), you could withdraw 4% of the balance (or $40,000) for 30 straight years, and you’d have a 96% success ratio. In other words, you’d have enough to live on, and your money wouldn’t run out. In fact, your portfolio balance would remain essentially unchanged.

Of course, this is a simplified view. These calculations don’t account for tax implications, inflation, emergency expenses, or times when the markets dip and cause portfolios to lose value.

But the big takeaway of this study is that generally speaking, if you can live off a 4% withdrawal from your portfolio, in most cases you will be financially secure in retirement.

Applying the 4% Rule

If you’re a Federal retiree, you’ll have your federal pension. (You’ll also have a supplement if you retire earlier than 62.) Then, beginning at age 62, you can turn on Social Security whenever you want. This gives two guaranteed monthly income sources–from Social Security and from your pension.

Now, add those amounts and subtract that total from your monthly expenses in retirement. This will show you how much additional money you’ll need to live on. Ask yourself, “Can I make up that shortfall by withdrawing 4% (or less) of the other money I’ve saved?” If the answer is “yes,” you’re in good financial shape.

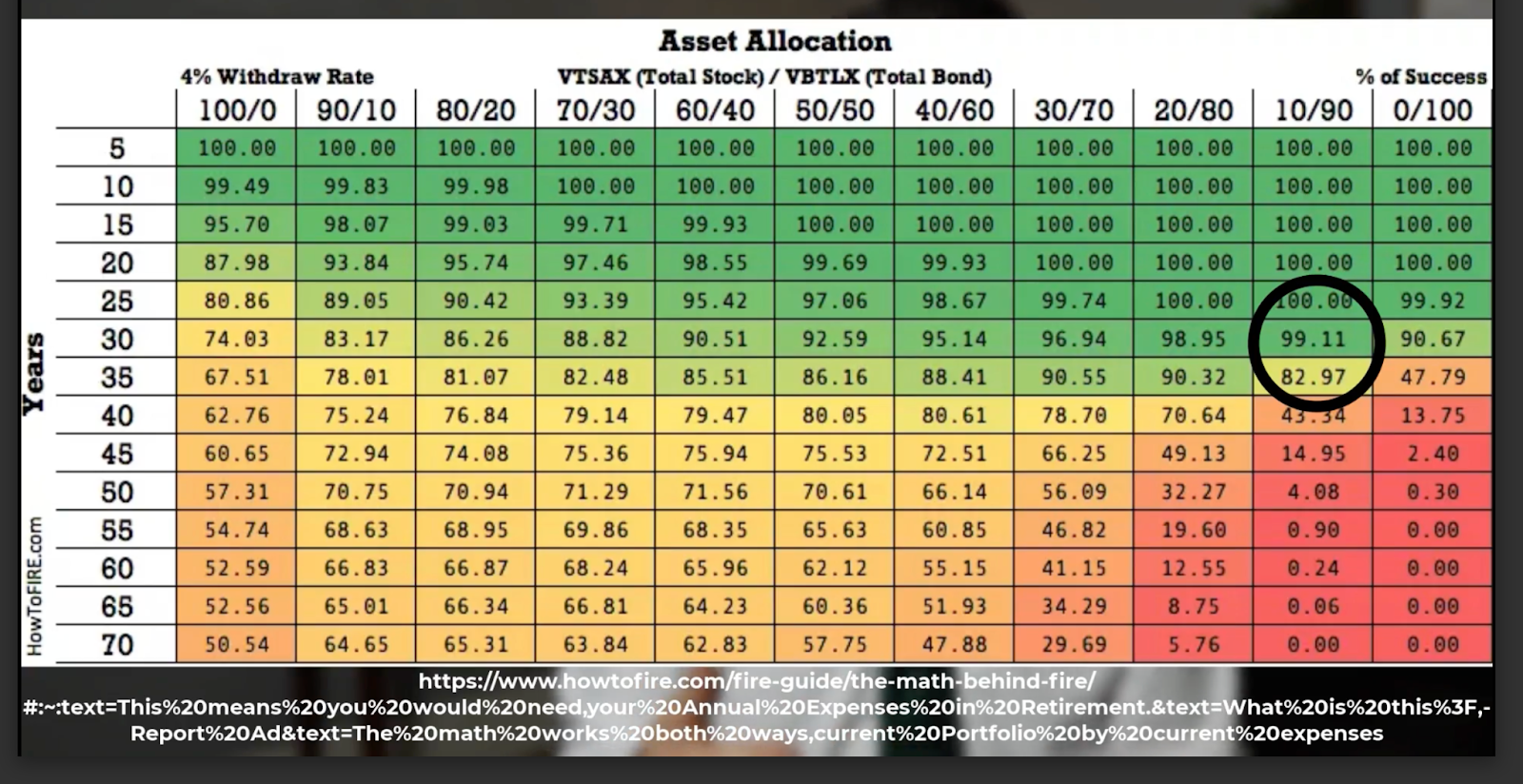

In another study, researchers used different portfolio percentages to try to answer the question, “What if a portfolio is more aggressive than a 50-50 mix?” Again they used 30 years as the benchmark.

As you can see in this chart, researchers got the highest success rate (99.11%) when they had only 10% of the portfolio assets invested in stocks and the remaining 90% invested in bonds.

They found a 50-50 combination over 30 years has a 92.59% success rate.

We have to remember that experiments and charts like this use a fixed percentage of withdrawal. They don’t take into account the need for “real-life flexibility.” The fact is, when the stock market is doing poorly, many people opt to withdraw less. And when the economy is humming people often feel comfortable withdrawing more.

Another option

Here’s another, and perhaps easier, way to apply the 4% Rule. Calculate your annual expenses in retirement. Subtract what you think your pension and/or Social Security will cover. Multiply the remaining balance by 25. That will give you the amount of money you need to have to be able to withdraw 4% annually.

So, for example, let’s say that after your pension and Social Security income, you still need $20,000 a year to meet your expenses. Multiply $20,000 times 25, and you get $500,000.

That’s the total you’ll need in order to make the 4% Rule work for you..

Again, use this 4% Rule as a guideline, a ballpark estimate. Don’t view it as a hard and fast guarantee. Stock markets are volatile. Interest rates change. Crises occur, and opportunities arise. Remember, there will always be tweaks you can make along the way to help ensure the success of your portfolio.

Other considerations

Remember that your expenses are every bit as important as how much money you’ve saved. When you’re able to spend less, you don’t need as much money to be financially free.

I’ve talked with people who accumulated $500,000–and realized that was enough to retire. I’ve also talked to folks with portfolios of $2 million and up…but based on the kind of lifestyle they wanted to enjoy in retirement, they didn’t feel it was enough. A lot is determined by how much you want to spend and what lifestyle you want to have in retirement.

Another takeaway from research by howtofire.com was that being a more aggressive investor does not necessarily make one’s portfolio last longer. You might assume that the more aggressive you are, the more likely it is you’ll have success over the years. But howtofire’s study showed a 98% success rate for 30 years with 10% allocated to stocks (also 20% and 30%). That’s relatively conservative.

We can’t forget taxes

Obviously, these studies–and the 4% Rule–don’t take into account various tax implications.

Again, let’s use the example of the person with a $1 million portfolio balance. The 4% Rule says they can withdraw $40,000 a year to pay their living expenses.

Now, if that money is in a Roth account (and they are over 59 and ½ and have had the account for five years) they can withdraw that 4% or $40,000 every year, tax-free. Awesome, right?

But what if those retirement assets are parked in a traditional TSP or traditional IRA?

That’s a different story. All the money in traditional accounts is taxable. Meaning, if they need $40,000 to live on, they will actually have to take out more than $40,000–a good bit more. Let’s say they’re in the 22% federal tax bracket and the 5% state tax bracket. That means they’ll really need to withdraw $54,794 each year in order to pay their tax bill and still have $40,000 to live on.

In other words, they won’t be withdrawing just 4% of their money. They’ll be withdrawing 5.4% of their portfolio! Over time, that extra 1.4% makes a big difference. It lessens the chance of their money lasting long-term.

When you’re starting out in your career, postponing taxes until retirement sounds like a sweet deal. Plus, you get that helpful tax deduction right away for whatever contributions you make to your traditional TSP or IRA. But many people get to retirement and are shocked to realize they actually need more assets (because each of their withdrawals comes with a hefty tax bill!

Again, because the 4% Rule doesn’t take into account individual tax implications, it’s merely a good rule of thumb, not an ironclad guarantee for every person.

If all this feels overwhelming…

The Rule of 4% offers a valuable starting point for retirement planning. But a comprehensive plan requires much more. You need to carefully evaluate your expenses, clearly understand your portfolio composition, and wisely consider present and future tax implications. All of this is critical in crafting a successful retirement strategy.

Because it can get complicated, many people seek the assistance of an experienced financial advisor.

That’s why we exist. At Christy Capital, we’re on a mission to help you take the mystery (and stress) out of retirement.

If you have $400,000 or more in retirement savings (in a TSP or IRA), and you’d like some expert help evaluating your accounts, double-checking your investment strategy, and settling on a retirement plan and withdrawal strategy that will work best for your situation, please reach out to us.

We can create a comprehensive financial blueprint for you. We’ll show you the income you’ll have with your pension and/or Social Security. And we’ll calculate the withdrawal amount you’ll need to fund the retirement lifestyle you want.

Simply visit our website and click on the green “TALK WITH AN ADVISOR” button on the upper right-hand corner of the page. Leave us your contact info, and we’ll be in touch right away.

Retirement planning is too important to mess up–and too critical to ignore. Please let us know how we can help you.